Cindy’s Column × Senior AI Money

Retirement money advice often sounds serious for a reason.

Protect your savings.

Control fixed expenses.

Watch inflation.

Plan for healthcare.

Avoid lifestyle creep.

All of that matters.

But there is another truth that matters too:

If your budget only protects survival and never protects joy, it starts to feel like punishment.

A lot of retirees do not overspend because they are careless.

They overspend because they never gave fun a proper place in the plan.

So the spending happens in a scattered way:

a lunch here

a gift there

an impulse day trip

another streaming subscription

a hobby purchase that “doesn’t count”

a weekend away that somehow ends up on the credit card

That is exactly why a joy budget works.

A joy budget is not reckless spending.

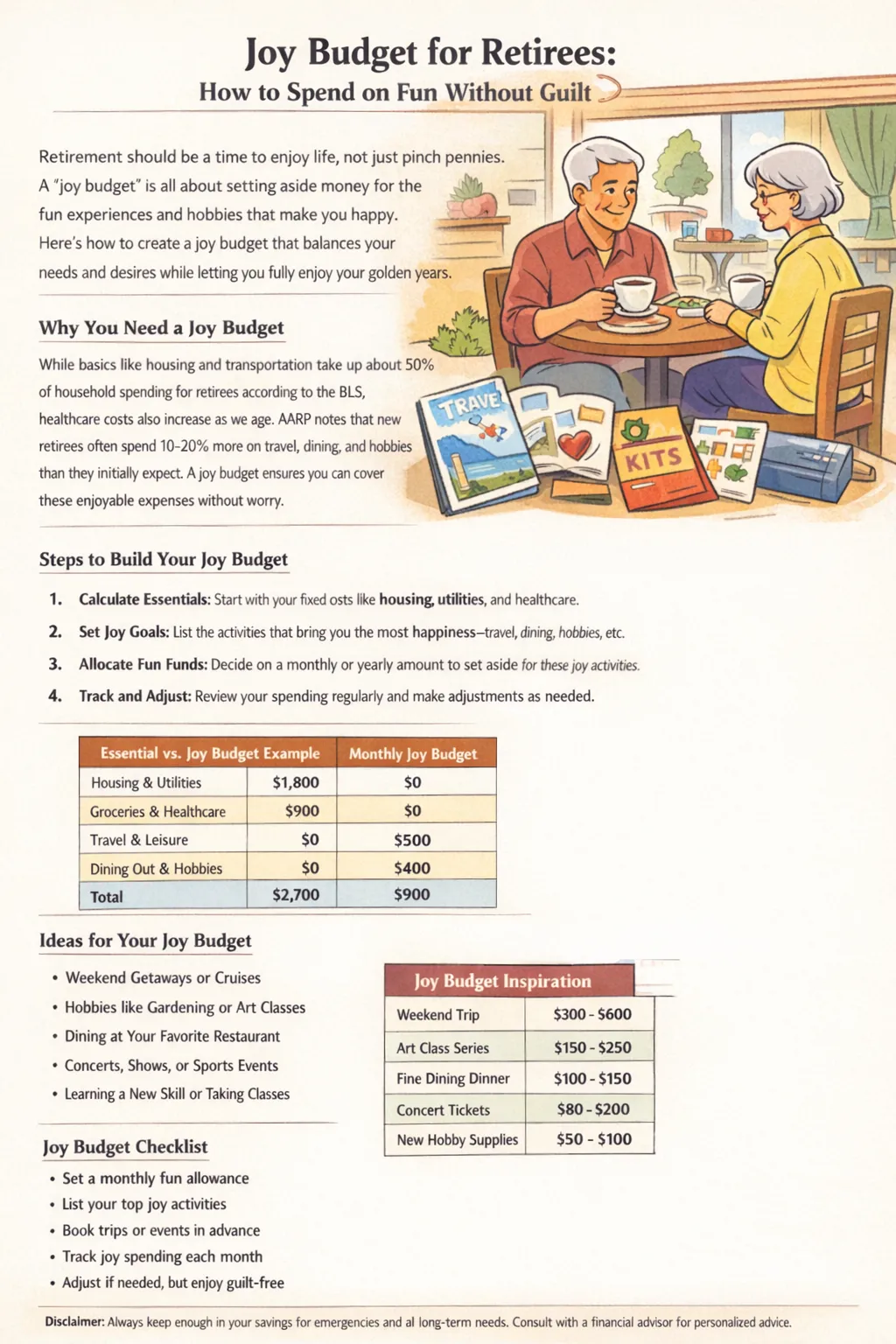

It is a small, intentional part of your retirement plan that gives money a job beyond bills, groceries, medication, and maintenance. It lets you enjoy retirement without pretending enjoyment is irresponsible.

That matters because housing and transportation still take a large share of household spending overall, and retiree households have historically spent a higher share of income on healthcare than average. At the same time, AARP notes that people in early retirement often spend 10 to 20 percent more on discretionary items than they expected.

The goal is not to spend more.

The goal is to spend on purpose.

What a joy budget really means

A joy budget is a pre-decided amount of money for things that make life feel lighter, warmer, more meaningful, or more enjoyable.

That can include:

coffee dates

hobby supplies

lunch out

movie tickets

short trips

gardening upgrades

family outings

craft classes

museum days

seasonal treats

small comforts that help you feel like life is still being lived

This is not the same as “miscellaneous.”

Miscellaneous spending usually leaks.

Joy spending should be named.

That is the key shift.

When joy gets named, it becomes easier to control.

When it is unnamed, it often becomes emotional spending disguised as “just this once.”

Why retirees need a joy budget

Retirement is not only a math problem.

It is also a lifestyle transition.

Your time changes.

Your routines change.

Your sense of reward changes.

For many people, work once provided structure, identity, and built-in treats:

the drive for coffee,

the lunch out,

the trip after a busy quarter,

the excuse to buy something useful.

Once retirement begins, spending can get strange.

Some retirees become so cautious that they stop enjoying money they can responsibly use.

Others swing the other way and spend freely because retirement feels like a long-delayed reward.

Neither extreme feels steady.

A joy budget helps because it creates permission with limits.

You do not have to ask every week:

“Can I afford this?”

“Should I feel guilty about this?”

“Am I being too tight?”

“Am I being irresponsible?”

You already decided.

That makes the spending calmer.

The joy budget rule

Fund joy after essentials, before random spending.

That order matters.

If joy comes before essentials, the budget becomes unstable.

If joy comes after random spending, joy disappears.

So the basic order is:

essentials

savings buffer

planned joy

everything else

This is especially useful in retirement because income may be fixed while spending is uneven.

Some months are calm.

Other months bring home repairs, healthcare bills, travel invitations, birthdays, or sudden family expenses.

A joy budget helps you protect a small quality-of-life amount without pretending every month will feel identical.

Part 1: Start with the real floor, not the fantasy floor

Before you can build a joy budget, you need a clear view of what your month already requires.

That means your true non-negotiables:

housing

utilities

groceries

insurance

medications

transportation

minimum debt payments

phone and internet

basic household supplies

Be honest here.

A lot of retirees underestimate their monthly floor because they forget irregular necessities like:

car registration

co-pays

home maintenance

gifts

pet care

seasonal clothing

annual subscriptions

appliance replacement

A joy budget only works when it sits on a realistic base.

If the base is too optimistic, joy money will get blamed later for problems it did not create.

Part 2: Decide what “joy” actually means to you

A useful joy budget is personal.

Not all retirees want the same things.

For one person, joy is travel.

For another, it is lunch with friends twice a month.

For another, it is taking grandchildren out for ice cream.

For another, it is fresh flowers, better coffee, art supplies, books, or music events.

That is why copying someone else’s retirement lifestyle is expensive.

The better question is:

What spending makes me feel most alive, most connected, or most restored?

Some joy spending gives a high emotional return for a low dollar amount.

Examples:

library café date

local garden center visit

baking supplies

museum membership

monthly breakfast with a friend

craft materials

small upgrades to a favorite hobby

Some joy spending is larger and needs planning.

Examples:

weekend travel

family reunion trip

concert tickets

seasonal classes

major hobby equipment

The point is not to eliminate joy.

The point is to choose the joy that matters most.

Table 1. Common joy categories for retirees

| Joy Category | Small Monthly Version | Planned Larger Version | Why It Works |

|---|---|---|---|

| Social joy | Coffee, lunch, cards, local meetups | Birthday dinner, small gathering | Supports connection |

| Hobby joy | Yarn, seeds, books, art supplies | Class series, equipment, workshop | Keeps the week interesting |

| Comfort joy | Better coffee, flowers, streaming, bakery treats | Recliner upgrade, patio refresh | Improves daily life |

| Experience joy | Museum day, day trip, movie | Weekend getaway, event tickets | Creates memories |

| Family joy | Treats for grandkids, shared meals | Holiday outing, family travel | Builds meaning |

| Health-linked joy | Pool pass, walking shoes, yoga class | Wellness retreat, fitness program | Supports energy and routine |

Part 3: Set one number, not ten vague promises

This is where many people get stuck.

They say things like:

I’ll just be careful.

I won’t eat out too much.

I’ll see how the month goes.

I’ll only spend when it feels worth it.

That sounds responsible, but it is not a real system.

A joy budget needs a number.

It can be monthly or annual.

Examples:

$100 a month

$250 a month

$400 a month

$1,200 a year for day trips

$2,400 a year for travel and fun

There is no magic number.

The right number depends on your cash flow, obligations, emergency cushion, and priorities.

A practical starting point is to choose a number small enough to feel safe and large enough to feel real.

If it is too tiny, you will ignore it.

If it is too big, you will not trust it.

AARP budgeting advice for older adults emphasizes separating discretionary from nondiscretionary expenses and building contingency room, which fits this approach well.

Part 4: Use “joy buckets” so fun spending does not sprawl

One joy budget can still feel messy unless you divide it.

Try three simple buckets:

Everyday Joy

Small weekly or monthly treats

Social Joy

Meals, coffees, outings, small gifts, events with others

Big Joy

Trips, tickets, larger hobby costs, family experiences

This matters because not all fun spending should compete with itself.

If one restaurant dinner wipes out the entire month’s fun money, the budget starts to feel harsh again.

Buckets make it easier to balance:

small pleasures now,

larger pleasures later.

Example:

$250 monthly joy budget

$80 Everyday Joy

$70 Social Joy

$100 Big Joy sinking fund

That means not every dollar must be spent this month.

Some of it can wait for the thing you truly care about.

Part 5: Stop guilt-spending and stop revenge-spending

Retirees often fall into one of two patterns.

Guilt-spending:

You buy something enjoyable, then feel uneasy, then over-correct by becoming extremely restrictive.

Revenge-spending:

You have been too strict for too long, then suddenly decide, “I’m retired. I deserve this,” and spend without structure.

Neither pattern is really about the item purchased.

It is about the absence of a plan.

A joy budget helps because it turns emotion into policy.

You no longer have to negotiate every pleasure from scratch.

You simply check:

Is it within the joy budget?

Does it fit this month’s plan?

Would I rather save this amount for a better joy purchase later?

That is a much steadier conversation.

Part 6: Use the “best memory per dollar” test

Not all joy spending is equal.

Some purchases feel expensive and forgettable.

Others feel modest and meaningful.

A strong retirement budget favors high-memory, high-value spending.

Ask:

Will I remember this next month?

Does this improve my week or just my mood for 20 minutes?

Does this fit my actual energy level?

Would I enjoy a simpler version just as much?

Am I buying joy or buying relief from stress?

That last question matters.

Buying joy and buying relief are not always the same thing.

If you are bored, lonely, anxious, or restless, spending can briefly feel like emotional treatment.

That is when the budget starts drifting.

The better goal is not “never spend emotionally.”

It is “notice what kind of spending this really is.”

Part 7: Real examples

Elaine, 68

Elaine and her husband were doing fine financially, but she felt guilty every time they spent money on anything “nonessential.” That created a strange pattern: months of extreme restraint followed by expensive restaurant weekends. They switched to a joy budget of $300 per month. They used $120 for social meals, $80 for local outings, and $100 for a travel sinking fund. After four months, Elaine said the biggest change was not the spending itself. It was the lack of self-argument.

David, 72

David lived alone and realized his random spending was not on luxury. It was on boredom. Convenience food, subscriptions he barely used, and impulse hobby purchases were quietly adding up. He replaced that with a $150 joy budget: $40 for coffee and reading outings, $35 for gardening, $25 for music, and $50 saved monthly for small trips. His spending became lower, but his enjoyment became higher because it was chosen.

Marsha, 64

Marsha had recently retired and wanted travel to be part of her life, but she did not want every trip to trigger anxiety. She created two levels of joy spending: $200 monthly for ordinary fun and a separate annual travel goal funded automatically. She discovered that small weekly pleasures actually reduced her urge for expensive “escape spending.” Her words were simple: “I stopped acting like joy had to be huge to count.”

Part 8: Plan joy around the calendar, not just the month

Some retirement spending is seasonal.

Spring may bring gardening and travel.

Summer may bring family outings.

Fall may bring hobbies, classes, and local events.

December may bring gifts and gatherings.

That means monthly budgeting alone can be too flat.

A better system is to look ahead 3 to 6 months.

Ask:

What fun expenses are likely coming?

Which ones matter most?

Which ones can I fund slowly?

This is especially relevant in 2026 because older adults continue to prioritize discretionary spending like travel while still being cost-conscious about it, according to AARP’s 2026 travel trends reporting.

So instead of pretending that joy is spontaneous, plan for it.

Planned joy usually feels better than panicked joy.

Table 2. Example joy budget by monthly income comfort level

| Monthly Cash-Flow Comfort | Suggested Joy Budget Range | Best Structure |

|---|---|---|

| Tight | $50–$125 | Focus on small recurring treats and free/low-cost outings |

| Moderate | $125–$300 | Mix of monthly joy and one sinking fund |

| Comfortable | $300–$600 | Social, hobby, and travel buckets |

| Very Comfortable | $600+ | Layered approach with annual experience planning |

This is not a rule.

It is a planning guide.

The best number is the one that protects both stability and enjoyment.

Checklist: Joy Budget Setup for Retirees

✔ List your true monthly essentials first

✔ Include irregular necessary costs before setting joy money

✔ Define what “joy” means for your life, not someone else’s

✔ Choose one monthly joy number

✔ Split joy into small buckets if needed

✔ Create a sinking fund for bigger experiences

✔ Track joy spending separately from groceries and bills

✔ Use low-cost joy on tired or quiet weeks

✔ Plan seasonal fun ahead of time

✔ Ask which purchases create the best memory per dollar

✔ Notice when spending is really stress relief

✔ Review the joy budget once a month without guilt

✔ Increase or reduce the number based on reality, not shame

✔ Protect emergency savings and major essentials first

✔ Let joy be intentional, not accidental

Part 9: What not to do

Do not call every unplanned purchase “joy.”

That turns the category into an excuse.

Do not make the joy budget so strict that it feels like punishment.

That usually causes backlash spending.

Do not compare your joy spending to wealthier retirees.

Someone else’s cruise habit is not your budget.

Do not assume low-cost joy is lesser joy.

For many retirees, routine pleasures create more happiness than occasional big expenses.

Do not forget that companionship, novelty, beauty, movement, and creativity all count as joy.

It is not only about travel.

EEAT note

This article is practical budgeting guidance for older adults and is meant to support thoughtful retirement spending, not replace individualized financial planning. It draws on current consumer spending data and retirement budgeting guidance showing that essentials remain heavy, healthcare can take a larger share for retirees, and discretionary spending can rise unexpectedly without a plan.

Final thought

A good retirement budget does not only keep you safe.

It keeps you human.

It makes room for connection, curiosity, pleasure, and memory.

A joy budget is not careless.

It is one of the cleanest ways to enjoy what you have without letting enjoyment quietly run the month.

Spend on purpose.

Save on purpose.

Enjoy on purpose.

Disclaimer

This article is for general educational purposes only and does not provide individualized financial, tax, investment, retirement-income, or legal advice. Retirement budgets vary based on income sources, savings, debt, health costs, family obligations, and risk tolerance. Readers should review their situation carefully and consult a qualified financial professional when making major spending or withdrawal decisions.

“`html id=”j4nqte” “