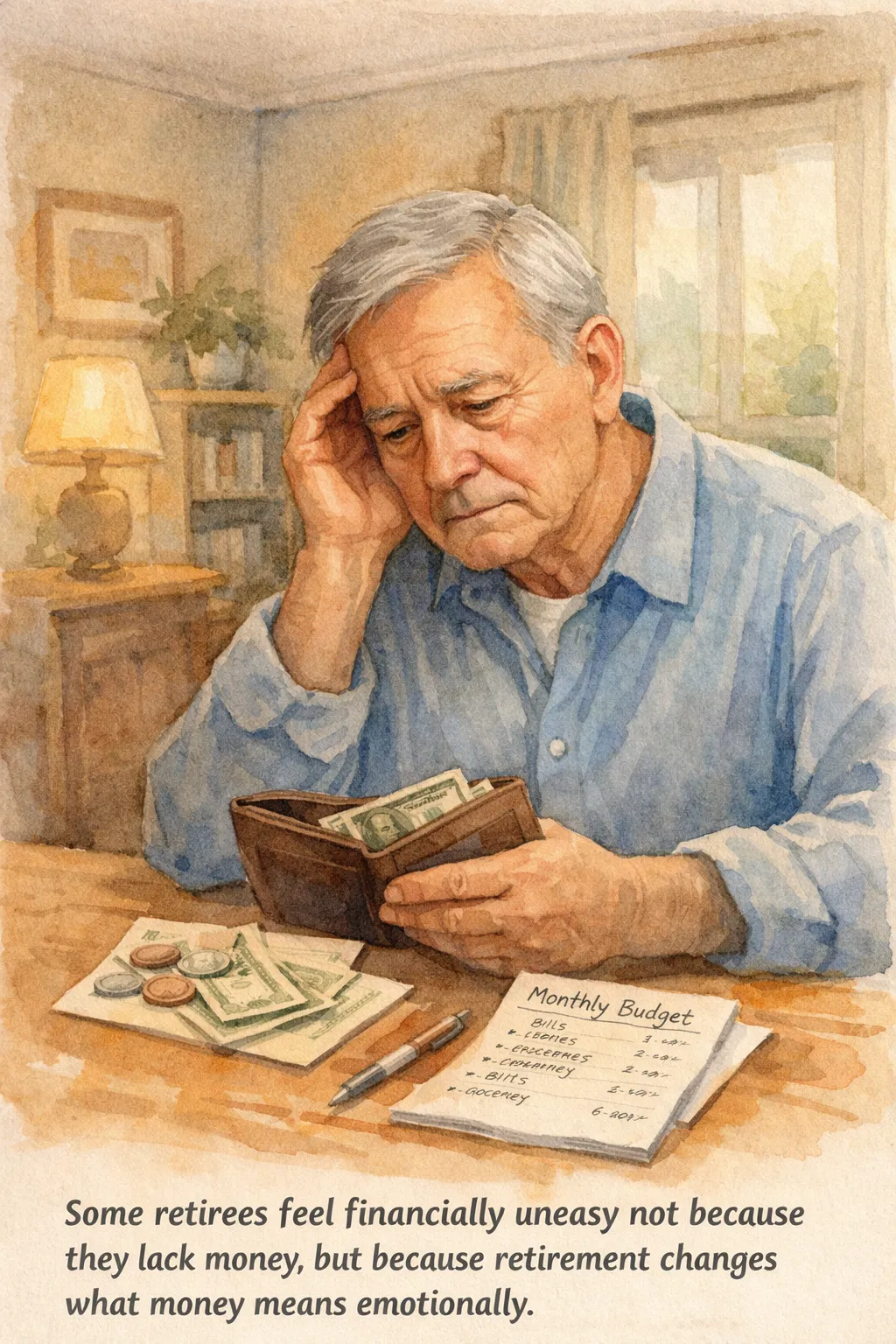

“I know I’m not broke… so why do I still feel financially uneasy?”

This is more common than people think after retirement.

On paper, things may look okay.

- the bills are being paid

- savings still exist

- there is no immediate crisis

- spending is not out of control

And yet, emotionally, something feels tight.

You hesitate before buying small things.

You check balances more often than you want to.

You feel uneasy spending money even when the spending is reasonable.

This experience can be confusing.

Because it is not always about actual poverty.

Sometimes, it is about the psychology of retirement money.

1. Income feels different when it stops being earned

Before retirement, money often felt connected to effort.

You worked.

You got paid.

You could recover from a mistake with future income.

After retirement, money feels different.

Now it can feel like:

- a fixed pool

- a limited runway

- something that only goes down

Even when your numbers are stable, your emotional experience of money changes.

That shift alone can make people feel poorer than they actually are.

2. Uncertainty feels expensive

Retirement money is rarely stressful only because of the amount.

It is stressful because of uncertainty.

Questions begin to stack up:

- What if prices keep rising?

- What if I need more care later?

- What if I live longer than expected?

- What if one big expense throws everything off?

These questions create a constant background tension.

So even when today is financially manageable, tomorrow feels expensive.

That emotional gap can feel like poverty, even when it is really uncertainty.

3. Spending now can feel like stealing from your future self

This is one of the biggest retirement money shifts.

Before retirement:

spending often felt normal if income continued coming in.

After retirement:

spending can feel like taking something away from the future.

That is why even reasonable purchases can trigger guilt.

You may think:

- “Do I really need this?”

- “What if I regret spending this later?”

- “I should probably save that instead.”

This mindset can become so strong that enjoyment disappears.

4. Past money stress does not disappear just because retirement begins

Many retirees carry old money emotions into a new stage of life.

If you spent decades feeling:

- cautious

- under pressure

- responsible for everyone

- worried about bills

- afraid of financial mistakes

Those patterns do not vanish automatically at retirement.

Sometimes the old stress remains, even when the current numbers are better.

Your bank account may improve faster than your nervous system.

5. Retirement removes the feeling of “margin”

A lot of retirees do not feel poor.

They feel like they have no margin.

Margin means:

room to absorb surprises.

Without margin, even stable finances can feel fragile.

A person may technically have enough money for monthly life,

but still feel anxious because there is not much extra space for:

- repairs

- medical changes

- family emergencies

- travel

- inflation

- care needs later on

That lack of breathing room is emotionally powerful.

6. Comparison quietly makes everything worse

Comparison changes retirement money feelings fast.

You may compare yourself to:

- friends who travel more

- neighbors who renovate more

- relatives who seem relaxed about spending

- people online who make retirement look effortless

This creates a distorted picture.

You stop asking:

“Am I safe enough for my actual life?”

And start asking:

“Why am I not as comfortable as them?”

Comparison often creates false scarcity.

7. The word “enough” becomes harder to define

Before retirement, enough may have meant:

- paying bills

- saving regularly

- avoiding debt

After retirement, enough becomes more emotional.

Now it may mean:

- safety

- predictability

- longevity

- freedom from fear

That is a much harder target.

And when the target keeps moving, it becomes easy to feel poor even while objectively stable.

Real-life example

Elaine, 70, had no debt, a paid-off home, and enough monthly income to cover her life comfortably.

But she still felt anxious buying new shoes or replacing small household items.

Her words were simple:

“I don’t feel broke. I feel exposed.”

That was the real issue.

Not lack of money.

Lack of emotional safety around money.

Once she created a small monthly “allowed spending” amount for everyday life, her stress dropped.

Nothing about her finances changed dramatically.

But her relationship with money did.

Another example

Martin, 73, kept checking his accounts every few days.

He was not overspending.

He was not in danger.

But he still felt uneasy.

Eventually he realized he was not checking for information.

He was checking for reassurance.

That distinction mattered.

Once he moved to a weekly money check instead of frequent balance checking, he felt steadier.

8. Feeling poor is sometimes really fear of future dependence

This is especially true for older adults living alone or thinking ahead.

Money anxiety is often connected to questions like:

- Will I need help later?

- Will I become a burden?

- Will I be able to choose my care?

- Will I lose control?

In this case, “I feel poor” may really mean:

“I’m afraid I won’t have enough control later.”

That fear deserves respect.

But it should be named accurately.

Because once you identify the real fear, you can respond more clearly.

9. What actually helps

The solution is not always “save more.”

Sometimes the real need is:

- more clarity

- less over-checking

- a realistic buffer

- a simple spending structure

- a better definition of enough

Helpful questions:

- What does “enough” mean for my real life?

- Which expenses are actually stable?

- Which fears are concrete, and which are vague?

- What would make me feel more financially steady this month?

These questions calm the nervous system more than constant account checking.

10. A calmer way to think about retirement money

Try separating money into three emotional categories:

1. Safety money

This covers essentials:

housing, food, utilities, insurance, medication

2. Stability money

This covers realistic irregular costs:

repairs, appointments, gifts, seasonal spending

3. Life money

This covers living:

coffee out, hobbies, outings, comfort purchases, small joy

Many retirees feel poor because “life money” disappears emotionally.

Everything starts feeling like it must stay in safety mode.

But a retirement life with no room for enjoyment often feels smaller than it needs to.

11. Signs this is more emotional than mathematical

You may be experiencing retirement money anxiety more than actual shortage if:

- you feel guilty spending small amounts

- you are financially stable but still feel constantly uneasy

- you check balances often for reassurance

- you postpone reasonable purchases repeatedly

- you struggle to define what “enough” means

- you feel safer saving than living

That does not mean the feeling is imaginary.

It means the solution may require emotional clarity, not only arithmetic.

12. A better question than “Am I poor?”

Instead of asking:

“Am I poor?”

Try asking:

“Do I feel unclear, unsafe, or out of control?”

That question is usually more accurate.

And it leads to better next steps.

Because those are not all the same problem.

Quick checklist

- I feel guilty spending even small amounts

- I often fear future costs more than current ones

- I check accounts for comfort, not just information

- I rarely feel like I have enough margin

- I struggle to enjoy money I can reasonably afford to use

If this feels familiar, the problem may not be lack of money alone.

It may be lack of emotional steadiness around money.

The key insight

Some retirees feel poor even with enough money

because retirement changes what money means.

It is no longer just income.

It becomes safety, time, control, and future security.

That is why the emotional experience can feel much tighter than the numbers suggest.

Conclusion

Feeling financially uneasy in retirement is not always a sign that you are doing something wrong.

Sometimes it means:

- you need more clarity

- you need a calmer money rhythm

- you need permission to define “enough” more realistically

Money peace in retirement is not just about having more.

It is about understanding what the money is carrying emotionally.

Once you see that clearly, the fear often becomes easier to manage.

Disclaimer

This content is for general educational purposes only and does not provide financial, legal, tax, or investment advice. Individual financial situations vary. For personalized guidance, consult a qualified financial professional.